In this article, we take a deeper look into the topics covered in our December 13th webinar: 3 Sustainability Topics to Watch in 2023: SEC Guidelines, Building Performance Standards, and Reporting Consolidation.

Where do the Proposed Mandatory SEC Climate Risk Disclosures Currently Stand?

What is it: On March 21 of this year, the SEC issued a proposed rulethat would enhance and standardize the climate-related disclosures provided by public companies. The aim is to provide quantitative and qualitative disclosures in a separately captioned “Climate-Related Disclosure” section that would immediately precede MD&A. These disclosures would address:

Scope 1, Scope 2, and Scope 3 GHG emissions

Climate-related risks and opportunities

Climate risk management processes

Climate targets and goals

Governance and oversight of climate-related risks

How was it received: More than 5,000 comments were submitted by the time the comment period closed in June, to be exact. The Commonwealth Climate and Law Initiative reviewed and summarized the comments as noted here. The majority of non-individual, substantive comments submitted are in support of the SEC’s proposed rulemaking. Trade associations were generally against or neutral on the proposal, with just 38 expressing support. Trade associations most often argued that: (i) the Proposal’s Scope 3 emissions requirements should be made less stringent or abolished altogether; and that (ii) the Proposal should require disclosures only of material climate-related information rather than require any disclosures without respect to materiality. Operating companies were relatively evenly split, while asset managers and “service provider” companies such as accountants, software firms, and consulting companies strongly supported the Proposal in general. Most substantive comments, irrespective of their position on the Proposal, were in favor of reporting standardization. The most frequently referenced frameworks in this regard were the TCFD framework, on which the Proposal is substantially based, the SASB standards and the ISSB standards.

Commonly cited issues with the rule:

Generally, companies had an issue with the level of complexity and impracticability of verifying Scope 3 disclosure requirements and very low data confidence around the collection of Scope 3 data. The proposed rule requires companies to disclose Scope 3 emissions, but only where an entity has a goal covering Scope 3 emissions or where material. Over 100 comments including asset managers/investment companies (such as CalSTRS and Oxfam America) and NGOs, generally supported broader Scope 3 disclosure. In contrast, over 200 comments reflected support for a narrower requirement where disclosures are material, and that the extent of Scope 3 disclosures should be limited to more easily quantifiable or estimable categories, or Scope 3 should be voluntary and/or delayed.

The other biggest issue is with materiality and the proposed 1% threshold for financial statement disclosures, under which climate change-related information would be disclosed in financial statements if that information could have at least a 1% impact on a line-by-line basis. The established materiality definition is set forth in the US Supreme Court’s 1976 decision, TSC Industries, Inc. v. Northway, Inc. where quote, Materiality occurs when there is a “substantial likelihood that a reasonable shareholder would consider it important in deciding how to vote.” At least 400 comments referred to the materiality concept. Trade associations, operating companies and NGOs, opposed the notion that firm-specific greenhouse gas emissions could be considered financially material. Others, in particular investors, identified climate risks and the disclosure of information on issuers’ progress towards climate goals as being material. The 1% threshold is cited as being too low and may lead to investors receiving immaterial information and confuse investors, rather than help them make informed decisions.

Latest news:Despite the fact that ESG reporting in general is heavily politicized on both sides in the US, there is still incredible momentum in policy when it comes to this topic going into 2023. Congressional inquiries will focus on whether ESG matters harm shareholders or violate fiduciary duty, and whether companies may be actually already be violating antitrust laws by participating in voluntary, industrywide ESG initiatives

The Biden administration announced its new proposed Federal Supplier Climate Risks and Resilience Rule, requiring federal government suppliers to disclose emissions and climate-related financial risk data, and to set science-based emissions reduction targets. The U.S. government is the world’s largest buyer of goods and services, with purchases reaching $630 billion last year. The new rules would require all federal contractors with over $7.5 million in annual contracts to report Scope 1 and 2 emissions, while contractors with over $50 million in annual contracts would also be required to publicly disclose relevant categories of Scope 3 emissions, as well as climate-related financial risks. Those contractors with greater than $50 million in contracts would also be required to set science-based emissions reduction targets. If implemented, the United States will become the first national government to regulate its supply chain by requiring government suppliers to disclose and reduce GHG emissions with the goal of achieving net zero emissions by 2050.

Takeaways: While the SEC rules will only apply to public companies, private companies are still likely to be held to the same standards as the effects of mandatory disclosure trickle down across supply chains and investor requirements. Additionally, 92% of S&P 500 companies already publish ESG reports mainly in response to reporting pressure from investors. In light of this, many companies are relieved that the SEC may standardize the current body of alphabet soup reporting frameworks and streamline an already quasi mandated process for them.

Monumental Changes in Sustainability Reporting Consolidation

ESG alphabet soup

In classifying different reporting functions, first are standards that govern the metrics based on specific rules for ESG measurement and disclosure. For example, GRI, SASB they effectively dictate what organizations must report. Frameworks are high-level guidelines that provide principles and guidance for how information should be disclosed. This would include frameworks like CDP, TCFD, etc. Finally, we have indices and ratings that provide the insights required for investors and companies to make more informed decisions and track ESG performance (SustainaAnalytics, Bloomberg, etc.). These are all built on globally agreed upon goals that provide a blueprint to build a sustainable future.

Consolidated reporting going into 2023

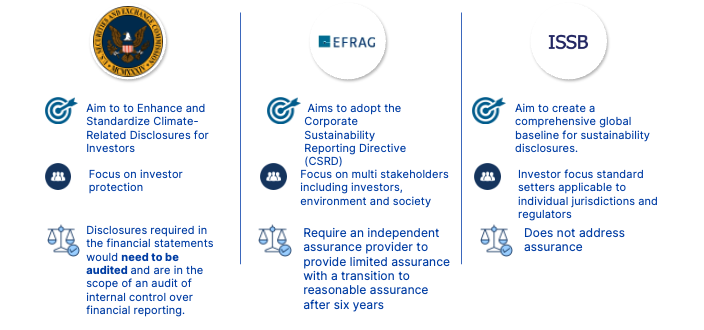

While many companies already make voluntary disclosures about environmental, social and governance (ESG) matters in separate sustainability reports, the regulators and standard setters are responding to calls from investors for more consistent, comparable information they can use to make investment decisions. 3 proposed sustainability disclosure standards aim to simplify the ESG reporting landscape:

In the United States, the Securities and Exchange Commission (SEC) in March 2022 issued a proposed climate disclosure rule that would require nearly all companies filing with the SEC to report on their climate-related risks, including greenhouse gas emissions.*

In Europe, on Nov 2022 the European Financial Reporting Advisory Group (EFRAG) approved the updated versions of the European Sustainability Reporting Standards (ESRS). The standards outline requirements for detailed corporate reporting on a broad range of environmental, social, and governance (ESG) issues.

On an international level, the IFRS Foundation’s recently-formed International Sustainability Standards Board (ISSB) released exposure drafts in April 2022 presenting detailed standards for climate-related disclosures. GRI will still exist on its own. But GRI and ISSB are collaborating to harmonize efforts, suggesting that the two standards “can be viewed as two interconnected reporting pillars that address distinct perspectives, which can together form a comprehensive corporate reporting regime for the disclosure of sustainability information. Similarly, the more climate-focused TCFD will continue to operate independently- while TCFD focuses primarily on making investor-focused recommendations for climate disclosures, SASB and GRI have a broader sustainability focus and are designed to meet the needs of stakeholders.

It is important to note that the SEC, EFRAG, and the ISSB each occupy very different spaces in the global regulatory landscape. The SEC’s focus is on the protection of investors in publicly traded companies in the USA. Unlike the SEC’s focus, which is strictly directed to investor protection, EFRAG’s proposals are based on the principle of double materiality. means that EFRAG’s proposed standards focus both on how sustainability matters impact reporting companies and also how reporting companies impact the environment and society. Finally, ISSB as a standard setter is the body that crafts sustainability standards that individual jurisdictions and regulators can adopt or otherwise use in their rulemaking.

Updates On the Growth of Building Performance Standards across the U.S.

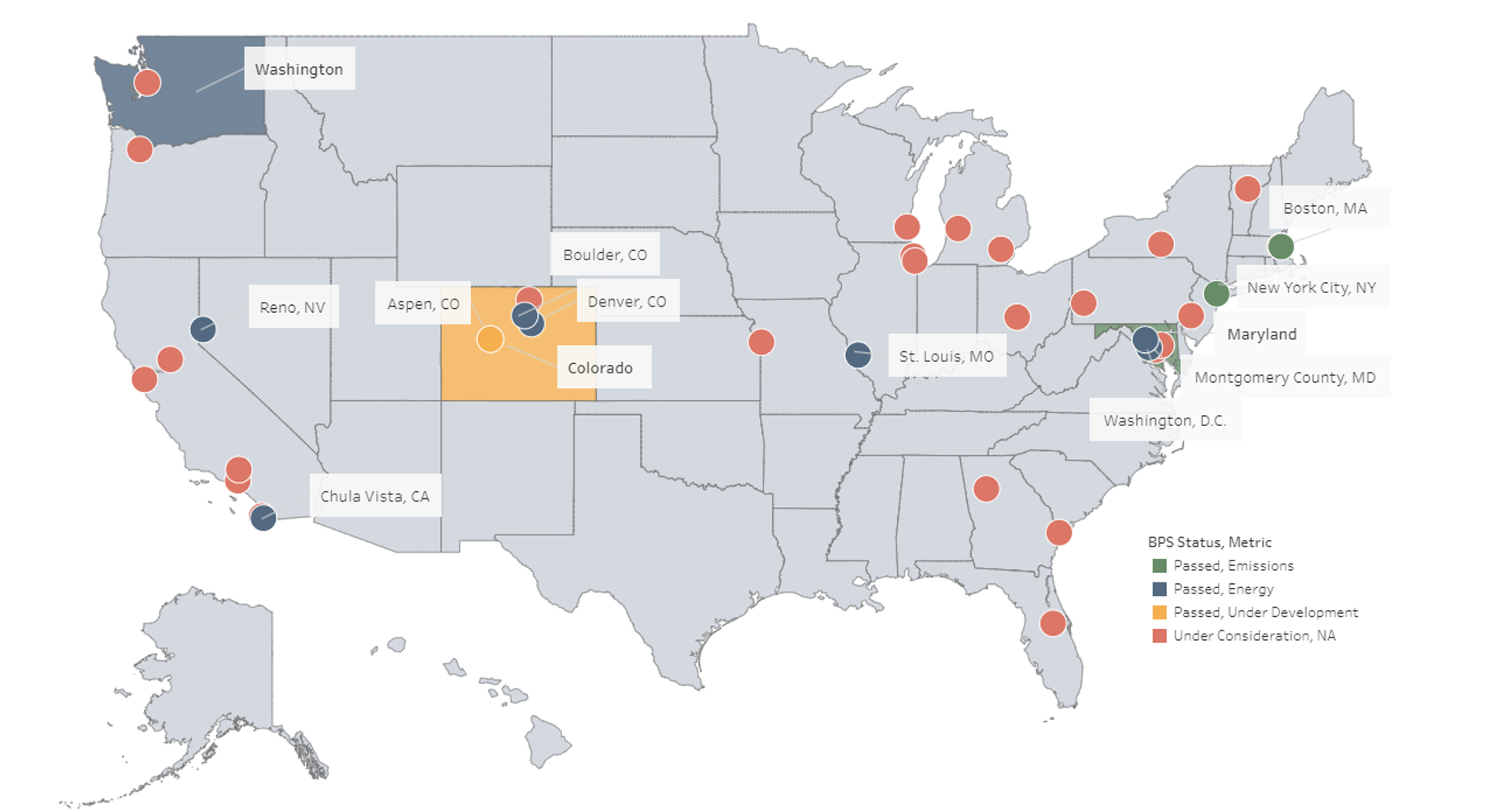

More than 45 cities, counties, and states have some sort of building energy benchmarking and transparency policy requiring reporting through ENERGY STAR Portfolio Manager. These are laws such as Local Law 84 in New York City, Building Energy Benchmarking Program in California, and the Energy Use Benchmarking Ordinance in Chicago. Building Performance Standards (BPS) are outcome-based policies and laws aimed at reducing the carbon impact of the built environment by requiring existing buildings to meet energy and/or greenhouse gas emissions-based performance targets. Unlike disclosure alone, a BPS establishes specific performance levels that buildings must achieve. By requiring buildings to meet a specified level of performance, a BPS can establish long-term certainty, helping building owners plan for upgrades that improve their buildings and, particularly important for the legislators, create jobs. So far 9 cities and 3 states have passed BPS, either regulating energy use intensity or emissions, with an additional 22 under consideration.

In January of this year President Biden launched the National Building Performance Standards Coalition, with 34 state and local government participants representing over 22 percent of the American population and ~20% of the building footprint. All these state and local governments have committed to inclusively design and implement equitable building performance standards and complementary programs and policies with a goal of adoption by Earth Day, 2024.

Earlier in December, a White House press call unveiled the first-ever Federal Building Performance Standard. The standard sets an ambitious goal to cut energy use and electrify equipment and appliances in 30 percent of the building space owned by the Federal government by 2030 in an effort to achieve net-zero emissions in all Federal buildings by 2045. According to the White House, upgrading the Federal building portfolio to meet the new standard will reduce reliance on imported fossil fuels from volatile parts of the world and cut millions of tons of GHG emissions.

Sustainability Preparation for the New Year

Reporting Frameworks: It’s going to be critical for companies to build processes that ensure high quality ESG data is captured beginning at least with their Fiscal Year 2023. All frameworks require companies to disclose Scopes 1 & 2 greenhouse gas emissions measured in metric tons of CO2 equivalent as prescribed by the GHG Protocol. Scope 3 emissions are required by the ISSB and ESRS proposals and are required by the SEC if Scope 3 emissions are material or if the company has set reduction targets that include Scope 3. The scope and audience of the proposals differ significantly with the SEC proposal being limited to climate change. The ISSB currently focused general requirements and climate disclosure provisions with an intention to expand to more ESG topics. The ESRS proposal covers the full range of environmental, social, and governance topics.

Educate your organization on the requirements of each disclosure

Evaluate existing processes and identify material topics that are most relevant to the company and its operational process throughout the value chain

Establish board-led governance structure and focus on aligning current reporting practices to TCFD framework (Almost all three proposals draw heavily on the framework)

Prepare for limited third party assurance with a longer-term transition to reasonable assurance likely under both the SEC and ESRS disclosure

Expand systems and engage with current process owner to identify sources of content and capture data required to meet the disclosure requirements.

Building Performance Standards: Once a BPS is passed, the reporting typically doesn’t start immediately, so in most cases no reports will be due in 2023.

As we wrap up 2022, it’s clear there’s a ton of momentum behind carbon accounting and sustainability reporting, with some uncertainty regarding the SEC proposal given the political environment. Regardless, the significant action from the city and state levels on sustainability presents a light at the end of the tunnel regarding reporting consolidation and significant changes on the way for all industries.

Navigating New AI Offerings Generative AI (GenAI) is set to revolutionize sustainability management by enhancing compliance, improving reporting accuracy, and streamlining resource allocation. Leaders in sustainability have recognized the transformative potential of GenAI to augment resource-stretched teams, enabling a sharper…

What Are Assertions and Audits? Audit and verification are the processes of examining and verifying the accuracy, completeness, and reliability of data and information and assurance is the deliverable or outcome of the audit. There are different levels of assurance,…

Key 2024 Updates for LL97 Compliance 1. New Reporting Platform: BEAM Building Energy Analysis Manager (BEAM) is now the main reporting portal for all LL97 submissions.BEAM will handle both annual (Article 320) and one-time (Article 321) compliance submissions. 2. Filing…

Log In

Log In

Top Sustainability Trends to Watch in 2025

Top Sustainability Trends to Watch in 2025