A 2024 GRESB Fact Sheet: Commonly Asked Questions and Best Practices for Score Enhancements

In an era where environmental, social, and governance (ESG) factors are critical to financial performance and societal impact, the GRESB Real Estate Assessment stands as a global benchmark for ESG reporting. It provides transparent and actionable data, setting the standard for listed property companies, private property funds, developers, and direct real estate investors. Evaluating performance across management, performance, and development, GRESB offers a comprehensive ESG rating, represented as a percentage with a maximum score of 100%.

Within the broader ESG landscape—characterized by many standards, frameworks, and rating agencies—GRESB serves as a crucial benchmark, providing investors and companies with valuable insights into their environmental responsibility, labor practices, and corporate governance. As organizations gear up for the GRESB submission deadline on July 1, 2024, we are pleased to present this factsheet.

The explainer offers a brief overview of GRESB and answers the questions:

What’s new with GRESB reporting in 2024?

What are the GRESB Score and Rating?

How does GRESB validate the data submitted in the assessment?

How does GRESB calculate data coverage?

How do we estimate consumption data for missing bills?

How do we accurately report asset-level waste data and manage data discrepancies that arise with asset-level reporting?

How do we report renovations and new construction projects?

How do we increase data coverage?

Benefits of reporting to GRESB

Additional resources that can help with GRESB reporting

What’s new with GRESB reporting in 2024?

This year, there have been moderate changes to the GRESB framework and significant updates to Tango Energy and Sustainability’s GRESB Reporting Module. Here’s a summary of the key changes for 2024:

Multiple Energy Ratings: Multiple energy ratings can now be reported per asset.

Building Certifications: The ‘Year’ field is now required.

EV Charging Consumption: Non-operational EV charging consumption must be reported separately from operational energy consumption.

Property Type Update: The property type has been updated from ‘Office: Medical Office’ to ‘Healthcare: Medical Office’.

Additional details about standard GRESB-related changes can be found on the GRESB website.

Enhancements to Tango Energy and Sustainability’s GRESB Reporting Module:

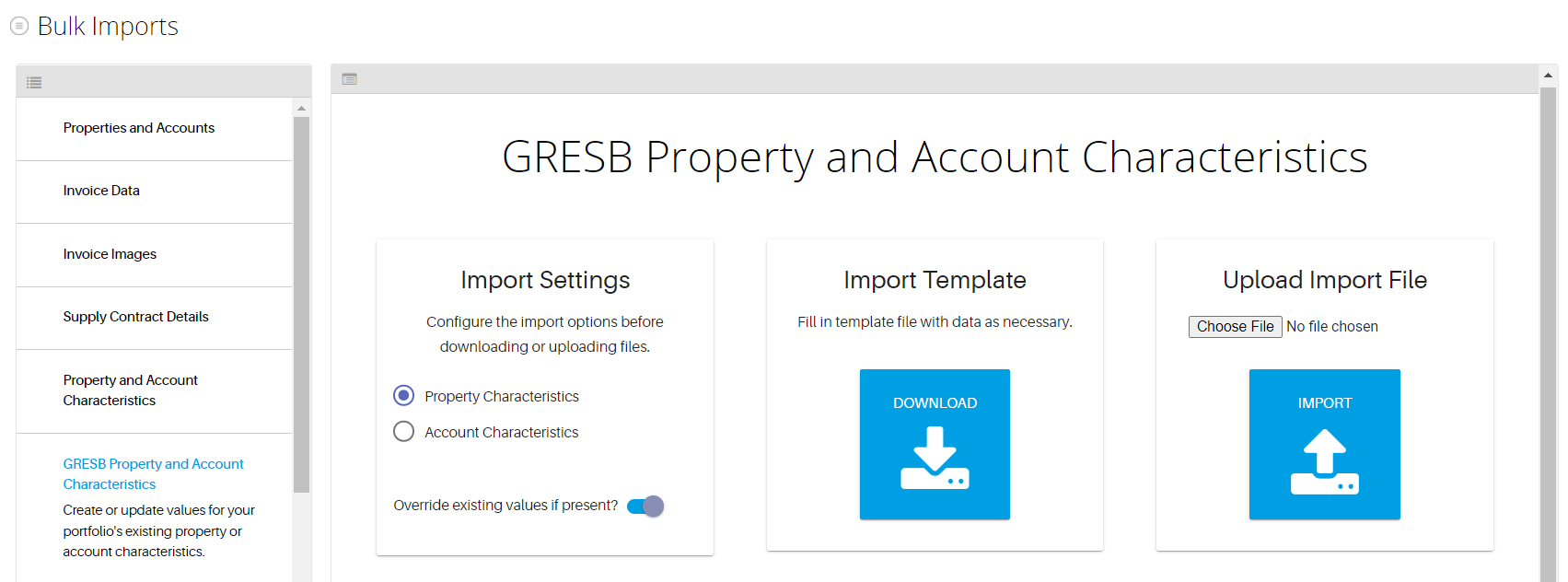

GRESB Characteristics Tab: A new dedicated tab lets clients maintain a detailed trail of asset-level GRESB-specific data.

Bulk Data Import: You can now bulk import data for all cells in an asset-level spreadsheet, streamlining data entry.

Effective Data Validation with Standardized Inputs: To increase data accuracy and reduce outliers and errors during checks, the platform has standardized values for floor area covered, date of reporting, etc.

The platform defaults:

Floor area covered = asset size

It automatically sets whole building = true

It automatically sets outdoor landlord controlled = false

It automatically sets outdoor tenant controlled = false

It automatically set hazardous waste = false (Refuse & Recycling accounts)

Comprehensive GRESB Data Configuration: The platform now offers comprehensive account-level characteristics that can be customized for different reporting years, ensuring flexibility and precision in data configuration for each year (e.g., 2022 vs. 2023).

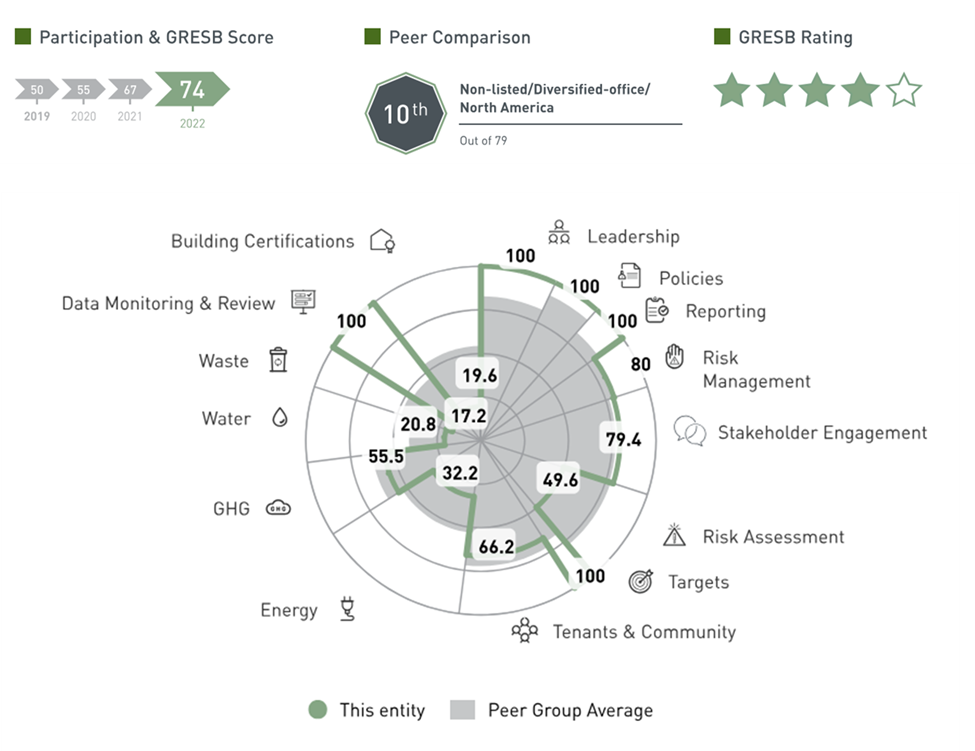

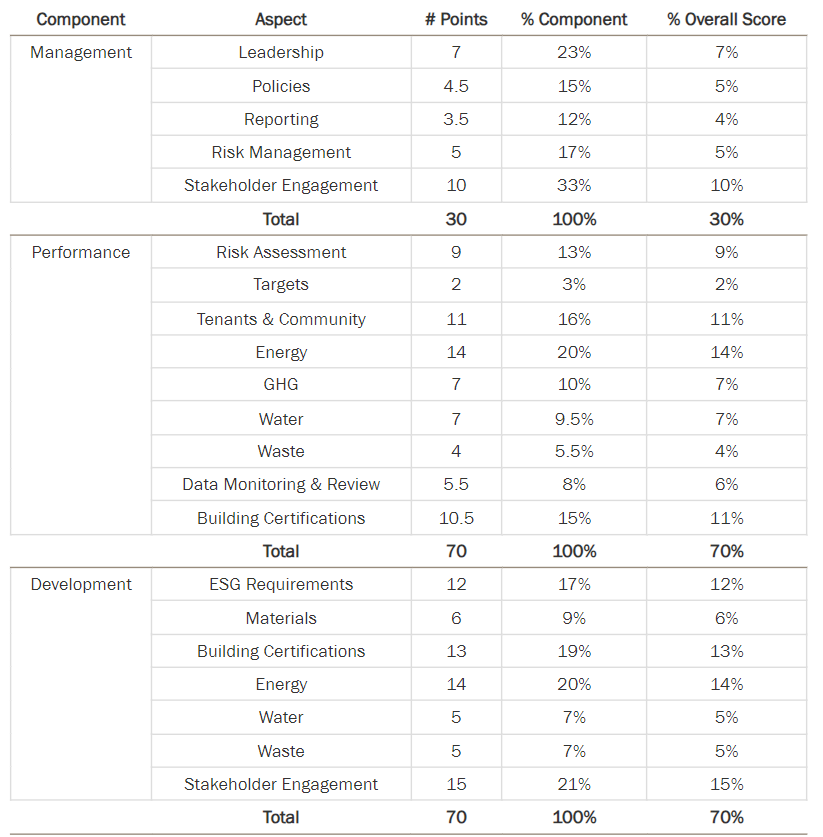

What are the GRESB Score and Rating?

Participants in the GRESB Assessment receive a Scorecard that summarizes their overall performance and provides detailed information on each GRESB Aspect. The Scorecard highlights absolute and relative performance and offers high-level insights into opportunities for improving ESG performance.

GRESB Score: The GRESB Score is an overall measure of ESG performance, represented as a percentage with a maximum score of 100%. This score provides quantitative insight into your ESG performance in absolute terms, over time, and compared to your peers. The GRESB Score is divided into two key dimensions:

Management & Policy (MP): This dimension evaluates how a company or fund manages and controls its portfolio and stakeholders and the policies and principles it adopts.

Implementation & Measurement (IM): This dimension assesses the execution of decisions and plans, and the measurement of actions related to the portfolio.

The score breakdown by the E, S, and G dimensions within each component is presented below.

GRESB Rating: The GRESB Rating is an overall measure of how effectively ESG issues are integrated into the management and practices of companies and funds. It is calculated relative to the global performance of all reporting entities, without considering property type and geography. This rating allows investors to differentiate the overall ESG performance of entities within the global property sector.

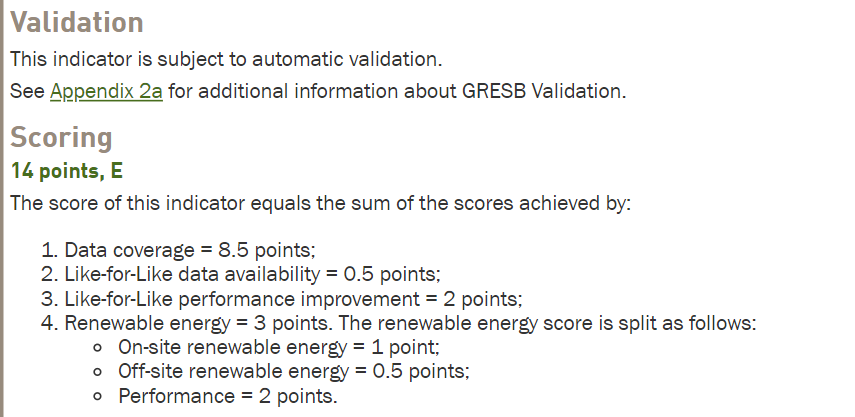

How does GRESB validate the data submitted in the assessment?

Validation can be structured into two categories: automatic validation and manual validation. It includes both automatic and manual checks to verify the existence, accuracy, and logical consistency of the data submitted.

Automatic Validation: Integrated into the GRESB portal, this process flags errors and warnings during data entry to ensure completeness and accuracy.

Manual Validation: After submission, independent third-party provider SAS conducts a detailed review of documents and text responses to ensure they are supported by sufficient evidence. GRESB sets and oversees the validation rules.

Existence Checks

Mandatory Fields: Ensure all mandatory fields in the asset spreadsheet are present.

Building Data: If the building is owned and operational during the reporting year, report Floor Area Covered and Maximum Floor Area for Energy, GHG, Water, and Waste, along with Data Availability and Vacancy Rate.

Date Checks

Reporting Year Compliance: Dates must fall within the reporting year (fiscal or calendar, as set in EC4).

Operational Control Logical Checks

Tenant Control: If “Whole building is Tenant Controlled” is selected, ensure “Whole Building” is also selected for Energy reporting.

Relevant Data: Only data in the Whole Building fields for energy and water are relevant when “Whole building is Tenant Controlled”; data in Base Building + Tenant Space fields will be ignored.

Floor Area Logical Checks

Maximum vs. Asset Size: Maximum Floor Area fields must be less than or equal to Asset Size.

Floor Area Covered vs. Maximum Floor Area: Floor Area Covered must be less than or equal to the corresponding Maximum Floor Area.

Sum Check: Sum of Maximum Floor Area fields for Energy, GHG, and Water must be at least equal to the Asset Size.

Consumption/Emission vs. Floor Area Covered

Consumption Values: If consumption values are reported, the corresponding Floor Area Covered field must be present and greater than zero.

Floor Area Covered: If reported, the corresponding Consumption/Emission field must be present.

Specific Rules

Energy:

Base Building + Tenant Space: Maximum Floor Areas must be less than or equal to asset sizes per subspace.

Renewable Energy: Consumed or purchased by the landlord must be less than or equal to the total consumption values in Landlord Controlled fields.

GHG Emissions:

Energy and GHG Tabs: Checks between Maximum Floor Area and Covered Floor Area fields.

Tenant Controlled: If the Whole Building is Tenant Controlled, only Scope 3 fields are allowed in the GHG tab, Maximum Floor Area must equal Asset Size, and Floor Area Covered must be less than or equal to the smaller of the Floor Areas Covered in Energy tab or GHG Scope 3 Maximum Floor Area.

Water:

Building Control: Data can be present for either Whole Building or Base Building + Tenant Space, not both.

Reused/Recycled Water: Purchased off-site must be less than or equal to the total reported consumption values.

Waste:

Data Coverage: If larger than zero, Hazardous and Non-hazardous Waste consumption fields must be present.

Disposal Routes: Sum of waste proportions by disposal routes must equal 100%.

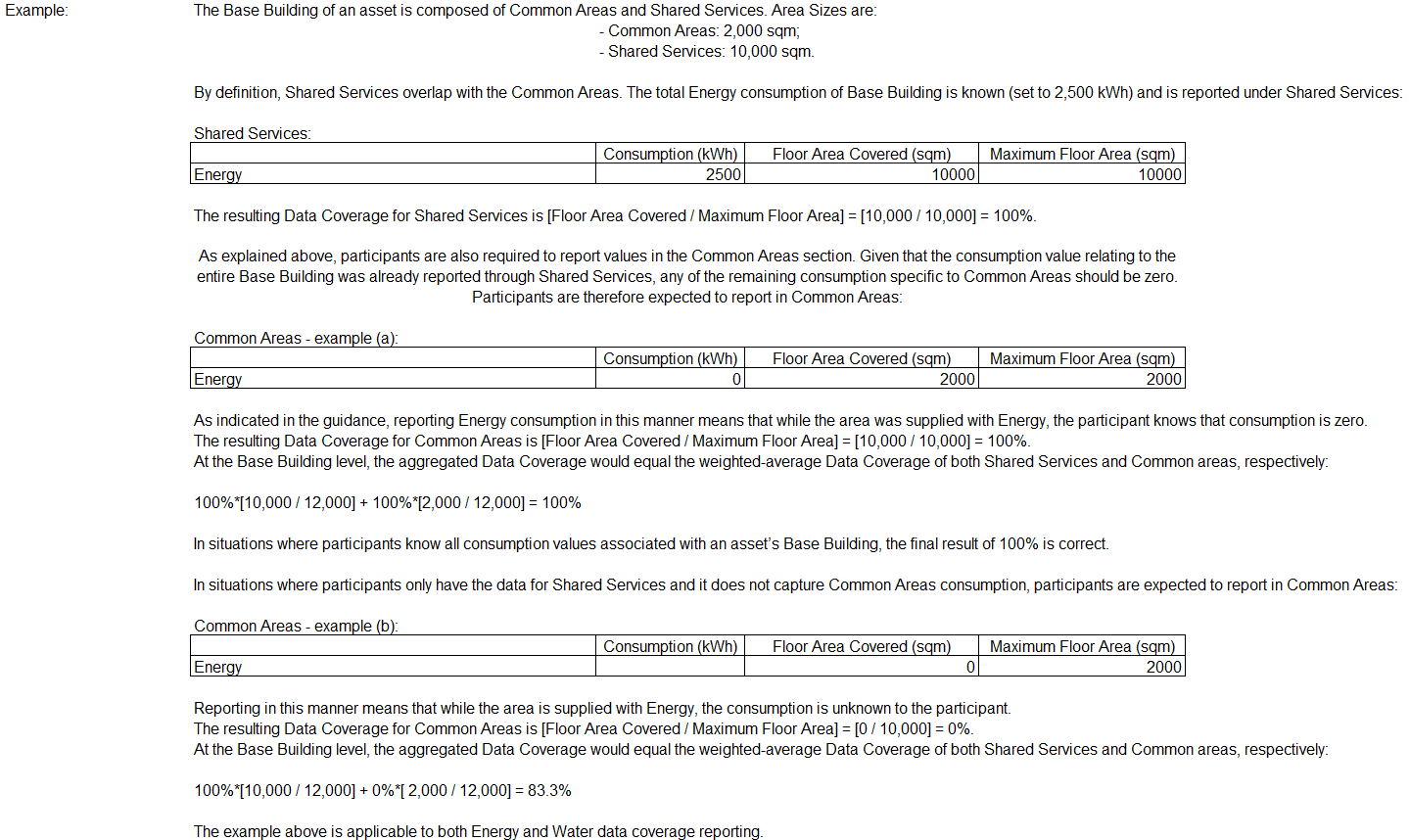

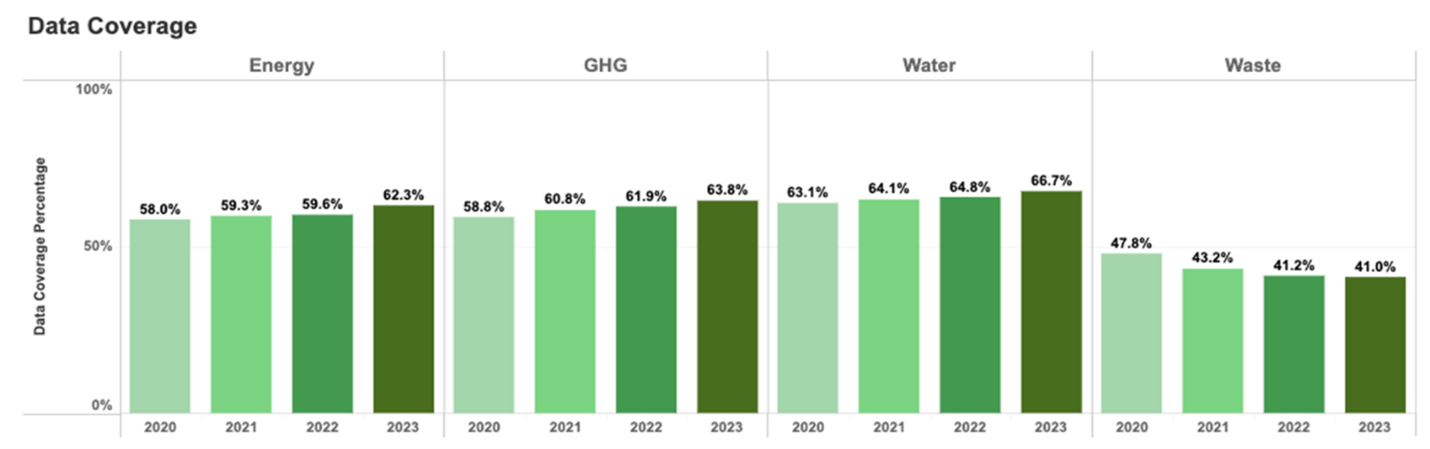

How does GRESB calculate data coverage?

GRESB calculates Data Coverage of operational energy based on the floor area for which consumption data is available and the total floor area where data could have been collected, known as the total supply area. Data Coverage is calculated separately for Whole Building, Base Building, and Tenant Space. It also accounts for the percentage of ownership reported at the asset level.

Data coverage percentages are scored separately for landlord-controlled and tenant-controlled areas across different property sub-types. The categories include: Landlord Controlled Areas (Whole Building, Base Building, and Tenant Spaces) and Tenant Controlled Areas (Whole Building and Tenant Spaces).

Example below demonstrates calculations for shared service:

How do we estimate consumption data for missing bills?

Participants are required to utilize actual data for Energy, GHG, Water, and Waste reporting. However, in cases where certain utility data is unavailable or deemed unreliable, estimates can be utilized under specific conditions:

Data Limitations:

Missing data must not exceed the lesser of:

20% of the total reporting period (up to 24 months).

Three months within a single reporting year.

Examples:

In a reporting year of 12 months where 10 months of data is known, participants are allowed to estimate a maximum of 2 months (2 / 10 = 20%).

If 5 months of data are known, the maximum allowable estimation is 1 month (1 / 5 = 20%).

If 21 months of data is known, participants are permitted to estimate a maximum of three months, as this is smaller than 20% of the actual data (20% * 21 = 4.2 months > 3 months).

Our dedicated analyst team begins by assessing the quality and quantity of client data and subsequently collaborates with clients to bridge any data gaps. To accomplish this, we utilize various methods such as applying estimates based on the same month in the prior year or calculating the average of existing invoices. Estimates then undergo approval from the client or assurance provider, ensuring accuracy in reporting. This approach enables clients to accurately report and leverage granular asset-level data effectively.

Estimates must align with the same scope, comprising the same aspect and area type. For instance, if energy consumption data is known for Tenant Spaces from January to May and July to December, it’s permissible to estimate June’s data within the same category. However, estimates are only acceptable under specific circumstances, such as invoicing delays, tenant data procurement delays, or meter reading issues; they cannot be used without a valid reason or if actual data retrieval is uncertain.

Additionally, utility data provided by official documentation from providers, even if estimated due to infrequent meter readings, is not considered estimated data. Reporting requirements mandate participants to disclose their estimation methodology, specify the proportion of total data estimated (not exceeding 20%), and provide reasoning for resorting to estimates. For waste data where actual tonnage is unknown, participants can use bin count, volume, and fill level to estimate, assuming full bins when fill levels are undisclosed. GRESB retains the right to verify compliance with estimation methodology, and failure to comply may prompt requests for data adjustment to maintain reporting integrity.

How do we accurately report asset-level waste data and manage data discrepancies that arise with asset-level reporting?

Accurate reporting of waste data at the asset level is crucial for property companies and funds to monitor environmental impact, assess process efficiency, and establish waste reduction targets. Information on hazardous and non-hazardous waste generation and disposal destinations provides valuable insights to manage environmental impacts and identify unnecessary financial burdens.

Requirements:

Participants must report waste generation and disposal route proportions at the asset level using the GRESB Asset Spreadsheet.

Note: Compost should be categorized under recycling.

Handling Discrepancies:

When annual consumption data is partially unavailable or unreliable, estimations may be necessary.

GRESB scores waste based on Data Coverage and Waste Management in the Real Estate Assessment. However, obtaining waste data, especially for tenant-controlled spaces, poses challenges due to factors like municipal waste collection management and data privacy concerns.

GRESB Approach:

GRESB recognizes these challenges and scores waste metrics separately for tenant-controlled and landlord-controlled spaces.

Benchmarking waste data separately ensures fair comparison among assets facing similar barriers.

Entities that successfully capture accurate data for tenant-controlled spaces can achieve more favorable benchmarking outcomes.

Best Practices:

Some participants have improved waste performance scores by partnering with waste management companies offering customized services beyond municipal collectors.

These services include waste monitoring, pickup, recycling, and disposal, overcoming operational control limitations.

How do we report recent renovations or new construction projects?

Scope of GRESB Reporting:

GRESB requires property companies and funds to report on their entire portfolio, including both Landlord Controlled and Tenant Controlled areas.

The Annual GRESB Assessment covers all assets held during the reporting year, regardless of sale or purchase.

Portfolio Classification and Reporting Components:

Standing Investments: Submit Management and Performance Components for a Standing Investments Benchmark Report, including a GRESB Score and Rating.

Development Projects: Submit Management and Development Components for a Development Benchmark Report, including a GRESB Score and Rating.

Both Standing Investments and Development Projects: Submit Management, Performance, and Development Components for separate Benchmark Reports.

Data Collection for Major Renovations:

GRESB requires data for properties under major renovations as part of the Development Component.

Major renovations involve alterations affecting over 50% of the building floor area or relocating over 50% of regular occupants.

New Construction activities, including enhancing property value, fall under this category.

Properties under construction at any time during the reporting year are considered for data collection.

Classification:

Major Renovations: Alterations affecting over 50% of the building floor area or relocating over 50% of occupants.

New Construction: Activities to obtain or change building/land use permissions and enhance property value.

Standing Investments: Completed properties owned for leasing and rental income production, regardless of occupancy level.

How do we increase data coverage?

GRESB partners with leading consultants, solution providers, and industry bodies across the globe to advance ESG in real assets.

WatchWire by Tango’s GRESB module provides the following benefits:

Enhancing Data Coverage and Simplifying Reporting: Achieving comprehensive data coverage is key to GRESB scoring success. Collaborating with a GRESB-affiliated premium data partner, such as Tango Energy & Sustainability, can significantly streamline the reporting process. Our software features a dedicated API connection to GRESB’s web portal, offering numerous benefits:

Extensive Coverage: 70% of GRESB reporting requirements are met using the platform’s building and portfolio data.

Streamlined Process: Automatically generate GRESB Real Estate Assessment responses from the platform’s data, covering most asset-level questions.

Enhanced Flexibility: Utilize tools like bulk data capture grids, location-level instructions, and account tagging to review, categorize, manage, and update responses before submission.

Support from GRESB AP-Certified Experts: Tackling GRESB reporting with a partner offers a range of resources, including informative webinars, customized resources, cheat sheets, and proactive communication, ensuring you are well-prepared at every stage. We will introduce a structured approach throughout the reporting season:

January: Tango’s Energy & Sustainability team begins by adding any additional sites, setting up utilities, and initiating data checks. Sites are allocated to funds and subgroups to ensure comprehensive portfolio representation.

April: With the opening of the GRESB portal, our specialists provide expert guidance for smooth data entry, including navigating lifecycle stages, occupancy details, and ownership percentages.

May and June: Focus shifts to data quality and intensity checks, with experts resolving any issues to ensure precise data for submission.

Benefits of Reporting to GRESB

GRESB gives an in-depth, all-encompassing analysis of the ESG performance of a company, fund, or asset. GRESB scores give you quantitative insight into your ESG performance in absolute terms, over time, against industry standards, and peer comparisons. The key benefits of the GRESB Real Estate Assessment are as follows:

Better understand the areas of the assessment in which you outperformed your peers

Identify areas of improvement best suited to your organizational needs and goals

Plan strategic changes to your process to ensure you maximize ESG efforts

GRESB is guided by investor and industry demands, ensuring material issues are being reported to encompass the sustainability performance of real assets

Aligned with international reporting frameworks, such as GRI, PRI, SAS, DJSI, TCFD, Paris Climate Agreement, UN SDGs, and region and country-specific climate disclosure

Navigating New AI Offerings Generative AI (GenAI) is set to revolutionize sustainability management by enhancing compliance, improving reporting accuracy, and streamlining resource allocation. Leaders in sustainability have recognized the transformative potential of GenAI to augment resource-stretched teams, enabling a sharper…

What Are Assertions and Audits? Audit and verification are the processes of examining and verifying the accuracy, completeness, and reliability of data and information and assurance is the deliverable or outcome of the audit. There are different levels of assurance,…

Key 2024 Updates for LL97 Compliance 1. New Reporting Platform: BEAM Building Energy Analysis Manager (BEAM) is now the main reporting portal for all LL97 submissions.BEAM will handle both annual (Article 320) and one-time (Article 321) compliance submissions. 2. Filing…

Log In

Log In

Top Sustainability Trends to Watch in 2025

Top Sustainability Trends to Watch in 2025