In this article, we will summarize the contents of our most recent webinar: 2023 Sustainability Reporting Frameworks Update: SASB, GRESB, and CDD, which can be viewed in the webinar section of our resource library. In this webinar, WatchWire’s senior sustainability analyst, Prerana Tirodkar, discusses a 2022 recap of new regulations and standards, and what to expect in 2023 for the upcoming reporting season.

Recapping 2022: 3 Proposed Standards

The regulatory environmental landscape continues to evolve every week. Before we jump into updates for 2023, it is essential to provide a short recap of events that defined the disclosure landscape in 2022.

In March 2022, the SEC issued a proposal on climate-related financial disclosures that would require nearly all companies filing with the SEC to report on their climate-related risks, including greenhouse gas emissions.

In Europe, on Nov 2022 the European Financial Reporting Advisory Group (EFRAG) approved the updated versions of the European Sustainability Reporting Standards (ESRS). The standards outline requirements for detailed corporate reporting on a broad range of environmental, social, and governance (ESG) issues

At the international level, the IFRS Foundation’s recently-formed International Sustainability Standards Board (ISSB) released exposure drafts “Exposure Drafts (EDs) IFRS S1 General Requirements for Disclosure of Sustainability related Financial Information” and “IFRS S2 Climate-related Disclosures” in April 2022 presenting detailed standards for climate-related disclosures.

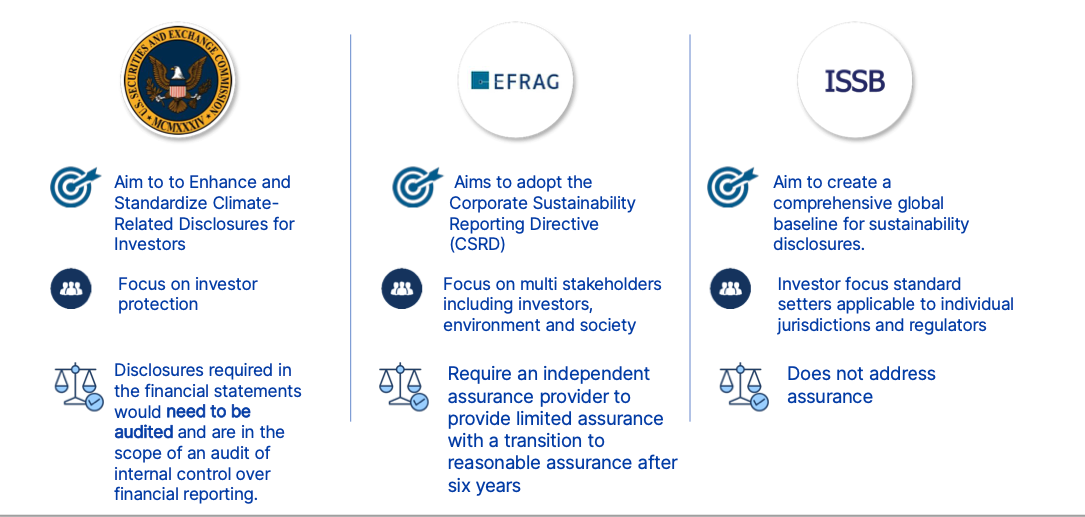

It should be noted that SEC, EFRAG, and the ISSB each occupy very different spaces in the global regulatory landscape.

The SEC’s focus is on the protection of investors in publicly traded companies in the USA.

EFRAG’s proposals are based on the principle of double materiality. means that EFRAG’s proposed standards focus both on how sustainability matters impact reporting companies and also on how reporting companies impact the environment and society.

Finally, ISSB as a standard setter is the body that crafts sustainability standards that individual jurisdictions and regulators can adopt or otherwise use in their rulemaking.

Harmonizing the Reporting Landscape:

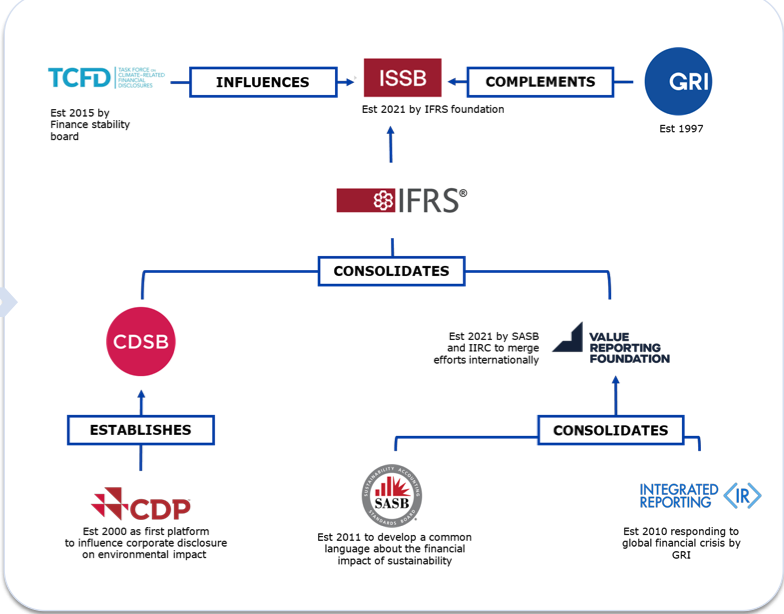

Increasing calls from companies to provide high-quality, globally comparable information on sustainability-related risks and opportunities led to the formation of ISSB in 2021.

ISSB builds on the work of market-led investor-focused reporting initiatives—including the Climate Disclosure Standards Board (CDSB), the Task Force for Climate-related Financial Disclosures (TCFD), the Value Reporting Foundation’s Integrated Reporting Framework and industry-based SASB Standards, as well as the World Economic Forum’s Stakeholder Capitalism Metrics.

The ISSB has set out four objectives:

developing standards for a global baseline of sustainability disclosures.

meeting the information needs of investors.

enabling companies to provide comprehensive sustainability information to global capital markets.

facilitating interoperability with disclosures that are jurisdiction-specific and/or aimed at broader stakeholder groups.

The GRI and more climate-focused TCFD will continue to operate independently. The difference between these three standards is that: while TCFD focuses primarily on making investor-focused recommendations for climate disclosures, SASB and GRI have a broader sustainability focus and are designed to meet the needs of many stakeholders. Thus two standards “can be viewed as two interconnected reporting pillars that address distinct perspectives, which can together form a comprehensive corporate reporting regime for the disclosure of sustainability information.

2023 Guidance

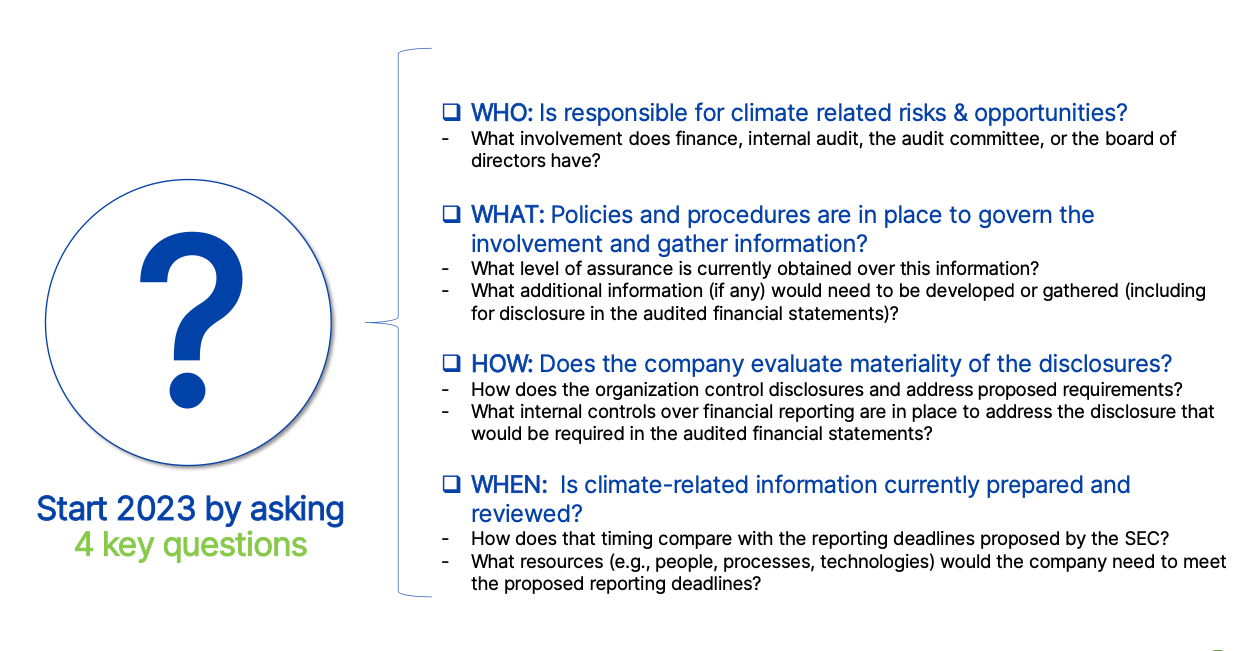

Preparing for sustainability reporting in 2023

Preparing for sustainability reporting in 2023 is going to be messy but the next few months are also going to see a lot of systemic shifts in the disclosure ecosystem. Currently on one hand after extensive consultation and many months of deliberations, the ISSB took its final decisions on the technical content of its initial two Standards in February 2023. Now the Standards will go through a thorough drafting and formal approval process, ahead of their issuance towards the end of Q2 2023. While on the other hand, CDP and GRESB questionnaires are now live for review.

SASB

SASB standards have transitioned to FRS Foundations International Sustainability Standards Board (ISSB). The ISSB will issue IFRS S1 and IFRS S2 in 2023 and is committed to supporting their implementation for businesses of all sizes and stages of development across different markets, although the effective date of the Standards is still to be decided.

Note that:

the ISSB is not just preserving the SASB Standards, it is updating and improving them to provide a solid footing when companies use them when applying the new IFRS Sustainability Disclosure Standards.

Therefore in the absence of specific IFRS Sustainability Disclosure Standards, ISSB has recommended that companies consider the SASB Standards to identify sustainability-related risks, opportunities, and appropriate metrics.

To prepare ahead of time, here are three ways that leading companies are laying the groundwork even before these standards are finalized:

Evaluate internal systems and processes for collecting, aggregating, and validating sustainability-related information across the organization and its value chain.

Consider the sustainability-related risks and opportunities that affect the business.

Review the ISSB’s proposed standards and supporting materials, including the SASB Standards, CDSB Framework, TCFD Recommendations, and the Integrated Reporting Framework to understand the needs

GRESB

2022 has been a transition year to establish the new GRESB Standards Development Process and for the GRESB Foundation to take on responsibility for setting the GRESB Standards. The changes for 2023 broadly cover Net Zero; Physical Climate Risk and Transition Risk; and Diversity, Equity, and Inclusion.

The key objectives for the 2023 Standards changes were to:

Focus on the most pressing issues, as expressed by global stakeholders through live engagement sessions and surveys

Maximizing the number of changes that could be reasonably achieved in the 2023 Standards

Minimizing the possible disruptions to participants, providing sufficient advance notice, and allowing participants to adequately prepare and adjust to the changes

Following the new process to prioritize, design, formalize, and validate the changes for 2023

CDP

The 2023 Questionnaires and Reporting Guidance are now available below. With a rise in adaptability, CDP will incorporate ISSB climate-related disclosure standards into the global environmental disclosure platform. The decision will improve the consistency of climate-related information for investors, and reduce the disclosure burden on entities through an alignment of requirements.

Understanding how emerging regulations and standards on sustainability compare

There are several key differences between the SEC’s proposed rule and the EC’s CSRD proposal.

First, the SEC’s proposed rule would mandate disclosure of climate-related information only, while the EC’s proposed CSRD would require companies to report on sustainability and climate-related information.

Second, unlike the SEC’s proposed rule, the EC’s proposed CSRD would mandate the development of a set of reporting standards (ESRS) with which companies (in the European Union) would be required to comply. The SEC based the disclosures prescribed in its proposed rule on the GHG Protocol and TCFD recommendations, but it has not proposed mandating any reporting standard with which companies would be required to align their disclosures.

Third, the scope of entities affected would differ: the EU requirements would extend to large nonlisted entities, while the SEC’s proposed rule would apply only to SEC registrants.

Lastly, the EU and U.S. proposed disclosures use a different focus for determining materiality.

(The SEC’s proposed rule and the CSRD proposal would both require assurance.)

ISSB’s proposed standards vs. EFRAF

ISSB’s proposed IFRS S1 standard focuses on general sustainability disclosures, and its proposed IFRS S2 standard focuses on climate-related disclosures. In contrast, the standards proposed in the EFRAG’s 13 EDs are collectively broader in scope, covering general principles and sustainability disclosure requirements as well as a wide range of topical disclosure requirements related to environmental, social, governance, and cross-cutting matters. When finalized, EFRAG’s proposed ESRS will be mandated in the European Union by a final CSRD. However, ISSB standards are not yet officially mandated by any jurisdictional regulations.

ESRS would require a stakeholder-focused double materiality assessment, which is the consideration of both (1) the material risks and opportunities of sustainability topics on the company’s value creation (financial materiality) and (2) the company’s material impacts on the economy, the environment, and people (impacts materiality). However, the ISSB’s proposed standards are geared toward investors and focus on enterprise value; therefore, the ISSB’s proposed materiality requirements are primarily focused on the users of general-purpose financial reporting.

The ISSB’s proposed IFRS S2 standard more closely aligns with the SEC’s proposed rule, in part because of the shared starting point — the TCFD recommendations — for the proposed disclosure requirements.

EFRAG’s proposed ESRS contains similar requirements that would align with the TCFD recommendations and meet the requirements of the SEC’s proposed disclosure rule; however, the proposed standards are organized in a different manner.

Where to Begin

The most common thread among the three key developments is that they aim to change the sustainability disclosure landscape moving forward. The SEC’s and EC’s proposals would mandate climate-related disclosure alongside and within annual financial filings. The ISSB’s proposed standards, once finalized, are expected to serve as the baseline standards for sustainability and climate disclosure and support future regulatory requirements across jurisdictions. Moving forward, sustainability reporting will need additional time and resources to mature to a level comparable to financial reporting such as requiring accelerated reporting timelines and enhanced governance and data management.

Look to TCFD and GRI for guidance on what will be included in ISSB, in addition to reporting on SASB standards as a way to prepare. It is also important to look into assurance as certain mandates and ISSB may start requiring 3rd party assurance in 2024 or 2025.

Navigating New AI Offerings Generative AI (GenAI) is set to revolutionize sustainability management by enhancing compliance, improving reporting accuracy, and streamlining resource allocation. Leaders in sustainability have recognized the transformative potential of GenAI to augment resource-stretched teams, enabling a sharper…

What Are Assertions and Audits? Audit and verification are the processes of examining and verifying the accuracy, completeness, and reliability of data and information and assurance is the deliverable or outcome of the audit. There are different levels of assurance,…

Key 2024 Updates for LL97 Compliance 1. New Reporting Platform: BEAM Building Energy Analysis Manager (BEAM) is now the main reporting portal for all LL97 submissions.BEAM will handle both annual (Article 320) and one-time (Article 321) compliance submissions. 2. Filing…

Log In

Log In

Top Sustainability Trends to Watch in 2025

Top Sustainability Trends to Watch in 2025