In this article, we take a deeper look into the activities that make up scope 3 emissions, and the challenges and nuances of calculating scope 3.

Emissions are classified into scopes for differentiating between direct and indirect emissions of a business and for more accurate measurement and reporting. Scope 3 emissions are indirect emissions (excluding purchased electricity, which is covered in scope 2) that are a consequence of an organization’s activities, but are not directly owned or controlled by the company. In essence, scope 3 requires a company to estimate the scope 1 emissions of all direct and indirect suppliers and customers. These emissions are often referred to as ‘supply chain emissions’ or ‘embodied carbon’ as they occur in the value chain of a company in activities like upstream and downstream transportation, business travel, and product disposal.

Although the majority of emissions in most supply chains are released in the initial stages of production within the extraction and processing of raw materials and fuels, the majority of businesses undergoing carbon accounting are not these raw materials providers. This complicates the accounting process as companies are finding it easier to engage in greenwashing behavior by avoiding the impacts of their upstream counterparts and suppliers since they are not directly associated with their own onsite processes. Scope 3 was created as part of the overall greenhouse gas emissions accounting process in order to address the disproportionate skew of emissions responsibility towards only a handful of companies. The CDP reporting standard uncovered that for most firms, scope 3 emissions will account for 5.5 times more emissions than their scope 1 and 2 emissions combined. A reminder that organizations must consider climate impacts beyond their direct sphere if they wish to make a difference.

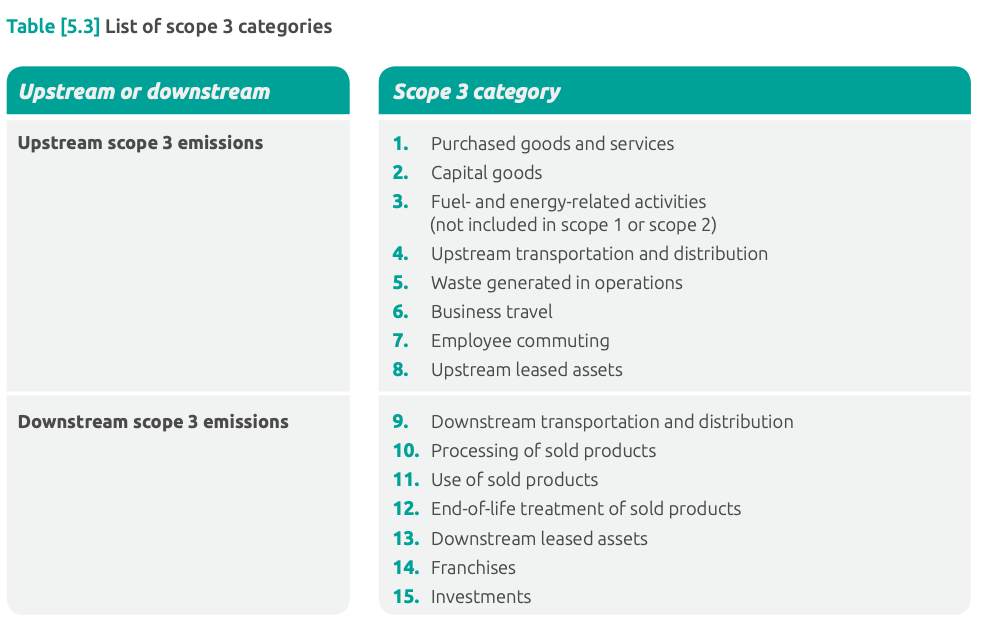

There are 15 categories of scope 3 that are divided into upstream and downstream activities.

Due to a wide range of challenges deterring or barring firms completely from accurate scope 3 calculations, this scope of accounting is not as widely adopted or even understood compared to scope 1 and 2 emissions accounting. The complexity of scope 3 accounting practices exceeds most current in-house capabilities, leading to the need for outsourcing help.

Gathering scope 3 data is more difficult than scope 1 or 2:To satisfy the extent of Scope 3 emissions, producers would need to report their own performance, as well as the performance of all suppliers, buyers, subcontractors, and other contributors to the product. Gathering accurate data from the fragmented production steps of multiple suppliers, locations, and downstream customers is an enormous task. Furthermore, suppliers and contractors are notoriously difficult to get ahold of in the first place, and once you do, there is no fail-safe way to ensure the accuracy of the emissions data that the suppliers end up giving you.

Inconsistencies across reporting frameworks and boundaries: The lack of a sector-specific framework to align accounting across the differences in various industries, and the conflicting interpretations among entities of scope 3 boundaries is enough to prevent firms from even attempting scope 3 accounting.

Despite a continued lack of consensus on the most effective way to account for scope 3, the GHG Protocol currently stands as the de facto global accounting method for measuring an entity’s direct, downstream, and upstream GHG emissions. This protocol defines methodologies for calculating and defining the scope of emissions, as well as informing the standard-setting criteria of many other reporting frameworks such as CDP, GRI, TCFD, SASB, and SBTi.

Although the GHG protocol method is widely embedded in many global climate agreements, many argue that the protocol falls short when it comes to its scope 3 standards. The protocol allows the use of industry average emissions data in place of primary data directly from each individual supplier when firms are in the process of estimating emissions for scope 3. This leads to rampant miscounting and data inaccuracy. Industry average data can reduce the emissions footprint of high-emitting firms by absorbing the efforts of low GHG-intensity firms in the same industry within the averages. Firms with carbon-intensive supply chain activities are therefore less incentivized to switch suppliers when instead they are able to greenwash with industry averages.

Is it required?

Companies that use the GHG Protocol are required to report Scope 1 and 2 emissions while reporting Scope 3 is voluntary but recommended. This holds true for many other sustainability & ESG reporting frameworks and standards as well. However, depending on firm size, certain regulatory bodies worldwide do mandate the disclosure of scope 3, albeit with an acknowledgment of inherent accounting errors that are likely to occur. In the U.S. the proposed legislation on climate-related disclosures from the SEC is set to provide fail-safe loopholes for scope 3 accounting, essentially acknowledging that these disclosures may be unreliable.

Is it relevant?

Despite challenges, Scope 3 value chain emissions are being reported now amongst corporations that want to decrease their negative environmental impacts and stay competitive where consumers are turning to greener brands. Investors are also shifting their resources to sustainable brands that are not only responsible in terms of their individual on-site production but engage with low emitting or net zero suppliers and customers as well.

Currently, most companies skip line item accounting of scope 3 emissions, which is not ideal, but sometimes necessary if scope 3 is a deterrent to begin calculation of easier scopes like 1 and 2. For the time being, defining which scope 3 emissions are most relevant (largest emitters, highest risk exposure, critical stakeholders, and potential reductions) might be a best practice instead of expending effort to gather comprehensive data from every single source in the supply chain. Corporates new to GHG accounting should begin with reliable scope 1 and 2 data and integrate scope 3 later on when better accounting standards are introduced or supply chain valuation data becomes available to you. Do not rely on opportunistic and unreliable scope 3 reporting based on inaccurate industry average data.

Solutions for reducing scope 3 emissions:

Focus on supply chain GHG reduction by working with low GHG intensity assets or suppliers

Carbon credits/ project development

Transportation electrification/ decarbonization

Resources:

The Greenhouse Gas Protocol has released extensive scope 3 guidance for calculations, boundaries, and emissions factors:

WatchWire provides full-service carbon accounting, tracking Scope 1, 2, and 3 emissions, renewable energy credits (RECs), global warming potential, and more. To discover more about WatchWire and its capabilities, you can visit our website, blog, or resource library, request a demo, or follow us on LinkedIn, Instagram, or Twitter to keep up-to-date on the latest energy and sustainability insights, news, and resources.

Navigating New AI Offerings Generative AI (GenAI) is set to revolutionize sustainability management by enhancing compliance, improving reporting accuracy, and streamlining resource allocation. Leaders in sustainability have recognized the transformative potential of GenAI to augment resource-stretched teams, enabling a sharper…

What Are Assertions and Audits? Audit and verification are the processes of examining and verifying the accuracy, completeness, and reliability of data and information and assurance is the deliverable or outcome of the audit. There are different levels of assurance,…

Key 2024 Updates for LL97 Compliance 1. New Reporting Platform: BEAM Building Energy Analysis Manager (BEAM) is now the main reporting portal for all LL97 submissions.BEAM will handle both annual (Article 320) and one-time (Article 321) compliance submissions. 2. Filing…

Log In

Log In

Top Sustainability Trends to Watch in 2025

Top Sustainability Trends to Watch in 2025