On March 6, 2024, Wednesday the SEC issued a final rule that requires registrants to provide climate-related disclosures in their annual reports and registration statements, including those for IPOs, beginning with annual reports for the year ending December 31, 2025.

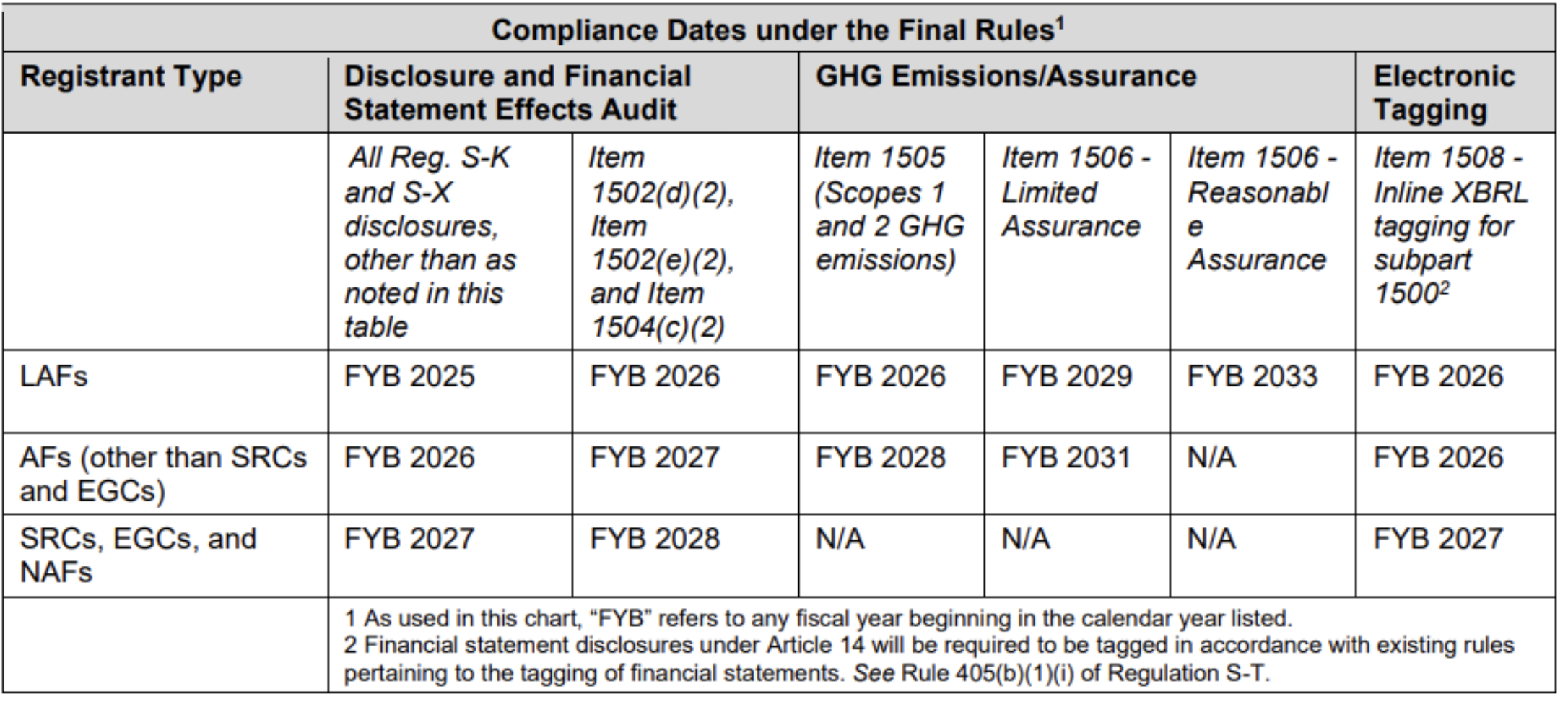

The final rules will become effective 60 days after publication in the Federal Register, and compliance will be phased in from 2025 to 2033.

Reporting Material Scope 1 and 2 Greenhouse Gas Emissions: Large Accelerated Filers (LAFs) and Accelerated Filers (AFs) will require disclosure of Scope 1 and/or Scope 2 greenhouse gas (GHG) emissions on a phased-in basis. Indirect Scope 3 GHG emissions are no longer included in the final reporting mandate.

Limited assurance and attestation reports will be rolled out over time: Assurance over Scope 1 and 2 emissions disclosures will be required, initially at a limited assurance level (within 3 years of initial GHG disclosures) and ultimately at a reasonable assurance level for LAFs (within 7 years of initial GHG emissions disclosures).

Disclosure of Climate-Related Risks: Registrants must disclose material climate-related risks, including actions taken to mitigate or adapt to these risks.

Board Oversight and Management’s Role: Information on the registrant’s board of directors’ oversight of climate-related risks and the role of management in managing these risks must be provided.

Climate-Related Targets or Goals: Disclosure of any climate-related targets or goals that significantly impact the registrant’s business, results, or financial condition is required. They should also disclose expenses, capitalized amounts, and losses related to carbon offsets and RECs used for climate-related goals. Any recovery from such events must be disclosed separately. If estimates for financial statements are materially impacted by weather risks or climate plans, a qualitative description of the impact on assumptions must be provided.

Disclosure of Financial Effects of Severe Weather Events: Registrants must disclose the financial impacts of severe weather events and other natural conditions, including associated costs and losses.

Who Does It Apply To:

The newly proposed climate rules apply to public companies with reporting obligations under the Securities Exchange Act Section 13(a) or Section 15(d), and companies filing a Securities Act or Exchange Act registration statement (together, registrants).

Timeline

Presentation of the disclosures

In the footnotes to the financial statements, registrants must disclose financial statement impacts and material impacts on their financial estimates and assumptions due to severe weather events and other natural conditions. Companies will also need to disclose a roll forward of carbon offsets and renewable energy credits or certificates (RECs) in the notes to the financial statements if carbon offsets and RECs are a material component of meeting their climate-related targets and goals.

Questions To Consider:

How do we operationalize data collection and use of technology to accurately measure, manage, and monitor our carbon footprint?

Have we conducted a thorough assessment to identify potential climate-related risks that could impact our operations, supply chain, or market position?

What are our climate-related targets, goals, and risks?

How do we build controls for non-financial reporting and what climate considerations are built into the governance structure of our company?

Effects of the Rollback of Scope 3 Emissions

While the SEC rule doesn’t enforce reporting on scope 3 emissions, they are important to investors’ understanding of transition risk. It’s strongly recommended to either continue tracking or start collecting data on them.

Here’s why:

Scope 3 emissions typically make up the majority, ranging from 65% to 95% of an organization’s carbon footprint, making them a business imperative for effective decarbonization strategies. By identifying and mitigating scope 3 emissions, businesses can improve operational efficiency, decrease environmental impact, and fortify resilience against regulatory shifts and market changes.

Adherence to evolving climate disclosure regulations like California’s SB253 and Europe’s CSRD might require scope 3 reporting, indirectly impacting businesses.

Defining Materiality

The rule proposes that companies report climate risks and emissions considered to have a material impact. But how do you define materiality? Materiality refers to the significance of an ESG issue to a company’s business and its stakeholders.

Imagine a retail chain operating numerous stores with high energy consumption and associated greenhouse gas emissions. If these emissions are substantial enough to influence investor decisions, compliance with environmental regulations, or public perception of the company’s sustainability efforts, or if they could result in fines or legal actions, they would be considered “material” emissions.

About the SEC

The U.S. Securities and Exchange Commission (SEC) is the regulatory body that oversees corporate disclosures and plays a pivotal role in shaping how companies communicate their financial risks to investors.

SEC Climate Disclosure Rules FAQ:

What is the climate disclosure rule?

In March 2022, the U.S. Securities and Exchange Commission (SEC) issued a new regulatory proposal that would mandate climate disclosure within financial reports for publicly-listed companies. The proposal focuses specifically on how climate risks are identified, assessed, managed, and disclosed; climate risk scenario analysis or the financial impact of severe weather and other natural events as well as transition activities; and greenhouse gas emissions (GHG). In short, calling for full transparency on plans to reduce carbon emissions and risks, and how companies are doing against those plans.

Much of the proposal is based on the TCFD framework with added detail like many other regulatory standards in Europe. Global disclosure mandates that also take guidance from the TCFD to be aware of include, the EU CSRD, UK SDR, and the global ISSB standards.

Why is the SEC involved?

The SEC’s purpose is to ensure that investors are provided with full, transparent, and truthful information that is deemed material to the financial bottom lines. Investors want to understand the climate risks of their investments and have been quasi-mandating such data for years. Because relevant sustainability information is now widely accepted and agreed upon as material to business financial risk, the SEC is attempting to formally standardize what is already occurring across the board: disclosing sustainability data. Rather than an attempt to uproot the long-standing business practices of corporations, the rule is intended to protect companies and investors alike by ensuring that everyone is asked the same questions and that all the answers are legally reliable and easy to find.

How Can Your Company Prepare?

Crossing the threshold from voluntary ESG/sustainability/ and climate risk disclosure to mandatory disclosure would invoke monumental shifts in capital markets and the business-as-usual operational strategies across all industries and company sizes as the ripple effects trickle down into smaller public and private entities.

To help your company prepare, we’ve created a Guide to the 2022 SEC Climate Disclosure Rules. This extensive guide outlines and clarifies what the robust regulatory document mandates, what to expect in terms of impacts of the regulatory changes, insights into why this shift in financial and sustainability reporting is occurring, and how to prepare as a corporate entity for the future of sustainability reporting.

About WatchWire

WatchWire by Tango is a market-leading, energy and sustainability data management platform that uses cloud-based software to collect, automize, and analyze utility, energy, and sustainability data metrics. WatchWire streamlines, automates, and standardizes your sustainability reporting process by integrating directly and/or providing reporting exports to ENERGY STAR Portfolio Manager, LEED Arc, GRESB, CDP, SASB, GRI, and more. The platform provides customizable dashboards, which allow asset managers, sustainability managers, engineers, and more to monitor individual key performance indicators (KPIs) and create custom views for specific use cases. WatchWire provides:

Automatic collection of energy, utility, sustainability, and emissions data through real-time metering. The data is then fully audited and organized in one place

GHG emissions tracking

Goal tracking (e.g., Net Zero, SBTi, waste diversion)

Carbon offset view of power purchases from the grid vs. on-site renewables generated vs. off-site RECs.

Opportunities to implement projects (track EEMs) and monitor distributed energy resource production (e.g. on-site solar)

To discover more about WatchWire and its capabilities, you can visit our website, blog, or resource library, request a demo, or follow us on LinkedIn, Instagram, or Twitter to keep up-to-date on the latest energy and sustainability insights, news, and resources.

California’s Climate Accountability laws originally consisted of three bills: Senate Bill 253 (the Climate Corporate Data Accountability Act), requires companies with revenues greater than $1 billion that do business in California to annually report their scope 1, 2, and 3…

1. Sustainability regulations are driving action around the world Throughout the week, we heard many different perspectives on how businesses are responding to and preparing for the many sustainability regulations and climate policies that are emerging around the world, including…

What are Green Leases? For those unfamiliar, a green lease incorporates clauses that foster collaboration between landlords and tenants on energy efficiency and environmental performance. These clauses range from general commitments to specific, enforceable obligations, ensuring shared responsibility for reducing…

Log In

Log In

California Signs Climate Laws, Bringing Back Urgent Timeline

California Signs Climate Laws, Bringing Back Urgent Timeline